In the 2024 Budget, the chancellor announced a cut to the higher rate of Capital Gains Tax (CGT) for residential property, which, on the surface, sounded like positive news for landlords. However, a reduced CGT allowance, known as the “Annual Exempt Amount”, could mean that many people selling a second property will face a higher tax bill than anticipated.

According to a survey carried out by Uswitch, around 3 in 10 landlords plan to sell a property during 2024. If you’re among them, understanding the potential tax bill you could face may be important.

You could face a Capital Gains Tax bill when you sell a property that isn’t your main home

CGT is a type of tax you pay when you sell certain assets and make a profit. Importantly for landlords, this includes residential properties that are not your main home.

During the March 2024 Budget, chancellor Jeremy Hunt announced that a cut to the higher rate of CGT on property would “boost the availability of housing by encouraging residential disposals”. If you’re a higher- or additional-rate taxpayer, the CGT rate you could pay on property gains fell from 28% to 24% for the 2024/25 tax year.

If CGT is due, the rate you pay will depend on the tax band(s) the taxable gains fall into when added to your other income. For 2024/25:

- If you’re a higher- or additional-rate taxpayer, your CGT rate would be 20% (24% on gains from residential property)

- If you’re a basic-rate taxpayer, you may benefit from a lower CGT rate of 10% (18% on gains from residential property) if the taxable amount falls within the basic-rate Income Tax band.

A 4% reduction in the rate of tax you pay might sound positive at first glance. However, the total gains you can make during a tax year before CGT is due has also fallen. As a result, some buy-to-let owners could find the CGT bill they’d face when selling is higher now than it was just a year ago.

The Annual Exempt Amount fell to £3,000 for 2024/25

In recent years, the government has slashed the CGT Annual Exempt Amount.

In 2024/25, you can earn £3,000 in gains before CGT might be due. Just two years ago in 2022/23, the Annual Exempt Amount was much more generous at £12,300. As a result, more people, including landlords who are selling property, are likely to find they’re liable for CGT in the coming years.

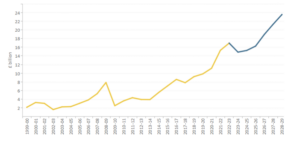

Indeed, forecasts from the Office of Budget Responsibility suggest the amount collected through CGT will be £15.2 billion – the equivalent of £530 for each household – in 2024/25. CGT receipts are predicted to reach £23.5 billion in 2028/29.

Source: Office for Budget Responsibility

So, for some property sellers, the reduction in the Annual Exempt Amount could outweigh the benefits of a lower CGT rate.

In fact, estate agents Hamptons estimate that almost 9 in 10 higher-rate taxpaying landlords will pay more CGT when selling property – even though the rate of tax has fallen. On average, a higher-rate taxpaying landlord is predicted to see their bill rise by £454 (4%).

The research adds that anyone “reporting gains of less than £68,000 will find themselves worse off”.

5 useful ways you could reduce your Capital Gains Tax bill when selling property

If you could face a CGT bill when selling property, there are some steps that might help you reduce it. Here are five practical steps that may be valuable to you.

- Own the property jointly. Owning property with another person or several people could effectively increase the gains you can make before CGT is due. For example, if you own the property jointly with your spouse, you’d be able to use both of your Annual Exempt Amounts. In 2024/25, in this scenario, it’d allow you to make gains of up to £6,000 before CGT may be due.

- Use the Private Residence Relief (PRR). If you’ve occupied the property at any point, you may benefit from a CGT reduction. For instance, if you purchased a property 10 years ago and had lived in it for the first five years, you could be entitled to relief to cover the gains you made during the time you resided in the property.

- Deduct costs from your gains. You may also be able to deduct costs associated with selling the property, such as solicitor or estate agent fees, from any gains. In some cases, you might also be able to deduct the cost for improvement work to the property, like an extension or boiler upgrade.

- Consider the timing of the sale. Second properties aren’t the only assets that could be liable for CGT. Other assets that you may need to pay CGT on include shares that aren’t held in a tax-efficient wrapper and personal possessions worth more than £6,000 (excluding your car). So, if you plan to dispose of several assets, considering the timing could be useful. You may want to delay a sale until a new tax year starts and your Annual Exempt Amount resets.

- Hold property in a limited company. For some landlords, holding property in a limited company could make sense. With this option, you wouldn’t be liable for CGT but may need to pay Corporation Tax, which could be at a lower rate.

Depending on your circumstances, there might be other ways you could reduce a potential CGT bill. Seeking tailored, professional advice could help you identify steps that are appropriate for you.

Contact us to talk about your buy-to-let property

If you have questions about your buy-to-let property, we could help. We could work with you to help you better understand a range of issues, from securing a competitive mortgage to calculating a CGT bill. Please get in touch to arrange a meeting.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

Your property may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.

The Financial Conduct Authority does not regulate buy-to-let (pure) and commercial mortgages.